MiCA Article 6: White paper translation rules for crypto issuers

- Apr 10

- 9 min read

Many compliance teams at crypto asset issuers assume they must translate their white paper into every language spoken across their marketing footprint. That assumption is both over-broad and potentially under-inclusive in ways that create real legal exposure. MiCA’s translation obligations are precise, jurisdiction-triggered, and tied to strict liability under Article 9. Getting the framework wrong means either wasting resources on unnecessary translations or, more dangerously, publishing non-compliant documents in host Member States where your asset is actively offered. This article breaks down what Article 6 actually requires, when translation is triggered, and how to maintain consistency across language versions without creating new compliance gaps.

Table of Contents

Understanding MiCA Article 6 and white paper content requirements

Language and translation rules: home state, host state, and international finance norms

Marketing versus public offering: When is translation actually required?

Multi-language white paper consistency: Quality control and XBRL tagging

What most compliance teams overlook about MiCA translation obligations

Key Takeaways

Point | Details |

Translation rules clarified | MiCA requires translation in host state languages only when there is a public offering or trading admission, not universally for all marketing languages. |

Home versus host | White papers must be published in the official language of the home state or a widely-used finance language, with host state rules applying for offers in their jurisdiction. |

Quality and consistency | Multi-version white papers demand rigorous quality control and XBRL tagging to avoid regulatory risks and ensure uniformity. |

Marketing nuance | Distinguishing between marketing and public offering is essential for compliance teams to avoid unnecessary translation obligations. |

Expert help available | Professional localization and multilingual compliance services are key for meeting MiCA requirements efficiently. |

Understanding MiCA Article 6 and white paper content requirements

MiCA Article 6 is the foundational obligation for any crypto asset issuer planning a public offering or seeking admission to trading on a regulated market within the EU. Before any offer reaches the public, the issuer must publish a white paper. This is not optional, and it is not a formality. The white paper is a legally binding disclosure document, and its contents are governed by Annex I of the regulation.

Annex I specifies exactly what must appear in the white paper. The required elements include:

Information about the issuer and the project

A description of the crypto asset and its underlying technology

Rights and obligations attached to the asset

Risks associated with the issuer, the asset, and the underlying technology

Information on the offer itself, including pricing and distribution

Details on the use of proceeds

A summary written in plain, non-technical language

The legal standard that applies to all of this content is that white paper information must be fair, clear, and non-misleading. That standard does not apply only to the original language version. It applies to every translated version published in connection with a public offering. This is where Article 9 becomes critical: issuers bear civil liability for inaccurate or misleading information in any language version of the white paper. A translation error is not a technicality. It is a potential liability trigger.

The definition of “offer to the public” under MiCA is also worth examining carefully. It covers any communication to persons in any form that presents sufficient information about the terms of the offer and the asset to enable an investor to decide whether to purchase. That scope is intentionally wide. If your distribution channel reaches retail investors in a host Member State, you are likely within the definition, regardless of whether you consider it a formal offer or a soft launch.

Understanding how a regulated document translation workflow connects to these legal standards is essential before you finalize your publication strategy. The content requirements and the liability regime are inseparable.

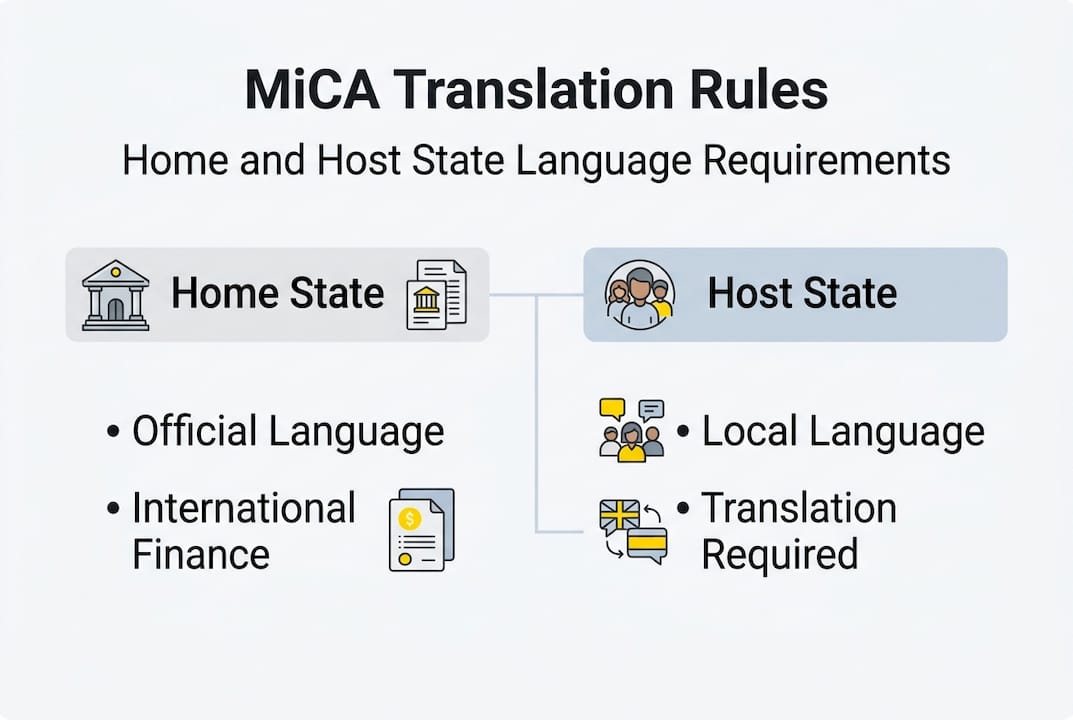

Language and translation rules: home state, host state, and international finance norms

Now that Article 6 content requirements are clear, let’s examine the intricate language rules for white paper publication.

MiCA draws a clear distinction between the home Member State and the host Member State. The home Member State is where the issuer is authorized or registered. The host Member State is any other EU jurisdiction where the crypto asset is offered to the public or admitted to trading. That distinction drives the language obligation.

For the home Member State, the white paper must be drawn up in the official language of that state or in a language customary in international finance. In practice, English functions as that international finance language for most issuers. A French issuer, for example, may publish its white paper in English for home state purposes if English is accepted as the customary finance language in its regulatory context.

For host Member States, the rule shifts. If you are offering the asset to the public in Germany, Poland, or Spain, you must provide a translation into the official language of each of those states, or again into the accepted international finance language if that satisfies local regulatory expectations. The key word is “if.” Host state competent authorities retain discretion, and some may insist on their official language for retail-facing documents.

Scenario | Language requirement | Translation triggered? |

Offer in home Member State only | Official language or international finance language | No |

Offer in host Member State | Official language of host state or accepted finance language | Yes, typically |

Marketing only, no public offer in host state | No specific MiCA translation requirement | Not automatically |

Admission to trading in host state | Same as public offer rule | Yes |

Pro Tip: Do not assume that publishing in English alone satisfies all host state obligations. Map each jurisdiction where you plan to offer or admit the asset to trading, then confirm with local counsel whether the competent authority accepts English or requires the national language.

The cross-border localization risk in crypto white papers mirrors what fund managers face under the Prospectus Regulation. The regulatory logic is the same: retail investor protection requires language accessibility. Compliance teams familiar with MiFID II translation compliance will recognize the pattern immediately.

Marketing versus public offering: When is translation actually required?

With language obligations covered, it’s critical to clarify when translation is actually triggered by marketing efforts.

This is the area where the most costly misunderstandings occur. Marketing activity and a public offering are not the same thing under MiCA, and the translation obligation is tied to the offer, not the marketing. Article 3(12) defines the offer to the public. Article 7 addresses marketing communications separately, and the two carry different obligations.

Here is how to think through the scenarios your compliance team will encounter:

Social media campaign in a host Member State, no white paper published yet. This is marketing. Translation is not yet triggered by MiCA’s white paper rules, though marketing communications must still be fair and non-misleading.

White paper published and asset offered to retail investors in a host Member State. Translation into the host state’s official language is required before the offer is made.

Asset admitted to trading on a platform operating in a host Member State. This also triggers the translation requirement, even without a separate retail marketing campaign.

Institutional-only distribution in a host Member State. MiCA includes exemptions for offers directed exclusively to qualified investors. Verify whether your distribution model qualifies before assuming translation is unnecessary.

“The distinction between marketing and a public offer is not always obvious in practice. Enforcement guidance remains limited, and competent authorities may interpret the threshold differently. Issuers should document their analysis and seek legal opinion before concluding that translation is not required in a given jurisdiction.”

The edge case analysis around ‘offer to public’ is particularly important for issuers using phased rollouts or waitlist models. If your waitlist communication contains pricing and asset details sufficient for an investor to make a purchase decision, regulators may treat it as an offer regardless of your internal labeling.

For regulated translation needs in this context, the stakes are high enough that generic tools are not appropriate. Compliance teams should also understand why public NMT tools create governance gaps that are difficult to defend in an audit or enforcement review.

Multi-language white paper consistency: Quality control and XBRL tagging

Once the translation trigger is clear, consistency across versions is equally important.

Publishing a white paper in three or four languages creates a new compliance risk: version divergence. If the German translation of a risk disclosure uses softer language than the English original, or if a technical term is rendered differently across the French and Spanish versions, you have created a material inconsistency. Under MiCA’s liability framework, that inconsistency is not a drafting error. It is a potential basis for investor claims.

Best practice | Common pitfall |

Use a single source document as the authoritative reference | Translating from intermediate versions rather than the original |

Maintain a centralized term base for all language pairs | Allowing each translator to choose terminology independently |

Apply XBRL tagging consistently across all language versions | Submitting untagged or inconsistently tagged data to regulators |

Conduct parallel QA review across language versions | Reviewing each language version in isolation |

Document the translation and review process for audit purposes | Relying on informal workflows with no audit trail |

XBRL tagging is now a material compliance requirement, not an optional technical enhancement. Multi-language white papers require consistency across versions, and XBRL tagging ensures that machine-readable data submitted to regulators is uniform regardless of the language version. ESMA has developed a dedicated taxonomy for MiCA reporting, and the taxonomy supports 24 EU languages for labels, which means your XBRL implementation must account for multilingual label sets.

For compliance teams, the practical checklist looks like this:

Lock the source document before any translation begins

Establish a master term base covering all regulated terminology in the white paper

Assign subject-matter expert linguists with financial regulatory backgrounds to each language pair

Run parallel quality assurance across all language versions before publication

Tag all structured data fields using the ESMA MiCA taxonomy

Retain documentation of every translation decision for regulatory audit purposes

The risk of SFDR translation errors illustrates exactly what happens when multilingual consistency is treated as a secondary concern. The same pattern applies here. And terminology consistency in Solvency II offers a useful parallel for how regulated entities manage this across complex, multi-jurisdiction document sets.

What most compliance teams overlook about MiCA translation obligations

Before wrapping up, let’s take a step back and look at what most experts miss about MiCA’s translation obligations.

The instinct to translate everything into every marketing language is understandable. It feels like the safe choice. But it can actually create risk by producing more language versions than your quality control process can reliably manage. More versions mean more surface area for inconsistency, more documents subject to MiCA’s liability regime, and more audit exposure.

The smarter approach is precision. Identify exactly where the offer to the public is triggered. Confirm with local counsel which languages are legally required in each jurisdiction. Then invest in translation quality for those specific language pairs rather than spreading resources thin across a broad, defensively motivated translation program.

Comparable EU regulatory frameworks, including the Prospectus Regulation and SFDR, have taught compliance teams that regulatory translation is a legal act, not a communication exercise. The same lesson applies here. A multilingual translation risk framework built on jurisdiction mapping, SME review, and documented QA is more defensible than volume-based translation with no governance structure.

MiCA enforcement is still maturing. Competent authorities are building their supervisory capacity. The issuers who will face the least friction are those who can demonstrate a structured, documented, legally grounded approach to their translation obligations, not those who translated the most languages.

Get expert support for your MiCA-compliant translations

MiCA’s strict liability framework leaves no room for translation errors in white papers published across EU jurisdictions. If your asset is offered in multiple Member States, each language version carries the same legal weight as the original.

AD VERBUM supports legal and compliance teams at regulated financial institutions with ISO 17100 and ISO 27001 certified translation workflows. Our AI+HUMAN hybrid process integrates your existing term bases and translation memories, applies proprietary LLM-based generation constrained by your regulatory terminology, and delivers subject-matter expert review by legal linguists with financial regulatory backgrounds. Everything runs on EU-hosted infrastructure with no public cloud exposure. Explore our localization services or learn how multilingual SEO supports compliant cross-border communication for crypto asset issuers.

Frequently asked questions

What triggers the MiCA white paper translation requirement?

Translation is required when a crypto asset is offered to the public or admitted to trading in a host Member State, as defined in Article 6. Marketing alone does not trigger the white paper translation obligation unless it constitutes a public offering.

Is English acceptable as a customary international finance language under MiCA?

Yes, English is generally accepted as a language customary in international finance for home Member State purposes, but host state rules may require the national official language for retail-facing public offerings.

How many EU languages are supported for MiCA taxonomy labels?

ESMA’s MiCA taxonomy supports 24 EU languages for labeling and compliance reporting, covering the full scope of Member State official languages.

Does marketing in another Member State automatically require translation?

No. Marketing communications and a public offering are legally distinct under MiCA. Translation is triggered by an offer to the public or admission to trading, not by marketing activity alone.

What steps can compliance teams take to ensure multi-language white paper consistency?

Teams should lock the source document before translation begins, maintain a centralized term base, assign expert legal linguists to each language pair, and apply XBRL tagging for machine-readable uniformity across all versions submitted to regulators.

Recommended